What Is a Health Insurance Broker? Definition, Role & Complete Guide

If you've ever tried to shop for health insurance on your own whether for yourself, your family, or your employees, you know how quickly it becomes overwhelming. Dozens of plans, confusing deductibles, provider networks that may or may not include your doctor, and premium costs that seem to change every year.

That's exactly the problem a health insurance broker solves.

A health insurance broker is a licensed professional who acts as your guide, your advocate, and your expert in the world of health coverage and in most cases, working with one costs you absolutely nothing extra. This guide covers everything you need to know: what a broker is, what they do, how they differ from agents and navigators, how they get paid, and how to find one.

What Is a Health Insurance Broker?

A health insurance broker is an intermediary between you (the buyer) and health insurance companies. Unlike a sales representative who works directly for one insurer, a broker is an independent professional contracted with many different carriers, meaning they can show you options from multiple companies and recommend whichever plan genuinely fits your situation.

Brokers are:

• Licensed by the state where they operate

• Contracted with multiple insurance carriers

• Legally required to act in your best interest in many states

• Paid via commission by insurance companies, not by you

• Certified to sell ACA marketplace plans and off-exchange plans

The health insurance market in the United States is enormous. There are hundreds of carriers and thousands of individual plans available across the country. The average person doesn't have the time, knowledge, or tools to compare them effectively. Brokers do this work as their full-time profession.

According to KFF (Kaiser Family Foundation), about 51% of insured Americans report difficulty understanding at least one aspect of their health insurance. That confusion around what's covered, what it costs out of pocket, and which providers are in-network is exactly where a broker adds value.

What Does a Health Insurance Broker Do?

A broker's work extends well beyond handing you a list of plan options. Here's a breakdown of what a health insurance broker actually does for their clients:

1. Conducts a Needs Assessment

Before recommending any plan, a good broker asks the right questions: How many people need coverage? What's your monthly budget? Do you have ongoing prescriptions or preferred doctors? Are your physicians in-network with certain carriers? This information shapes every recommendation that follows.

2. Shops the Market on Your Behalf

A broker pulls quotes from multiple insurance companies simultaneously. Where you might spend hours on insurer websites comparing premiums and coverage tables, a broker runs this analysis in minutes using professional tools — and they know what the comparison numbers actually mean.

3. Explains Your Options in Plain English

One of the most valuable things a broker does is translate insurance jargon into plain language. Terms like deductible, copay, coinsurance, out-of-pocket maximum, HMO, PPO, HDHP, and HSA all have specific meanings that affect how much you pay. A broker explains exactly what each plan means for your specific situation.

4. Guides You Through Enrollment

Whether you're enrolling through the ACA marketplace, a state exchange, or directly with an insurance company, a broker handles the paperwork. They ensure your application is submitted correctly and on time during open enrollment or a qualifying special enrollment period.

5. Provides Ongoing Support Year-Round

This is where brokers truly earn their keep. After enrollment, a broker remains your point of contact for claims questions, billing disputes, plan changes, and annual renewals. Most people don't realize that when you have a problem with an insurance claim, you can call your broker they advocate on your behalf with the insurer.

6. Helps Businesses Manage Group Plans

For businesses, a group health insurance broker handles the entire employee benefits process: researching plans, presenting options to leadership, managing open enrollment for employees, tracking compliance with ACA requirements, and renewing the plan annually. HR teams at small and mid-size companies often rely on brokers to manage this entire function.

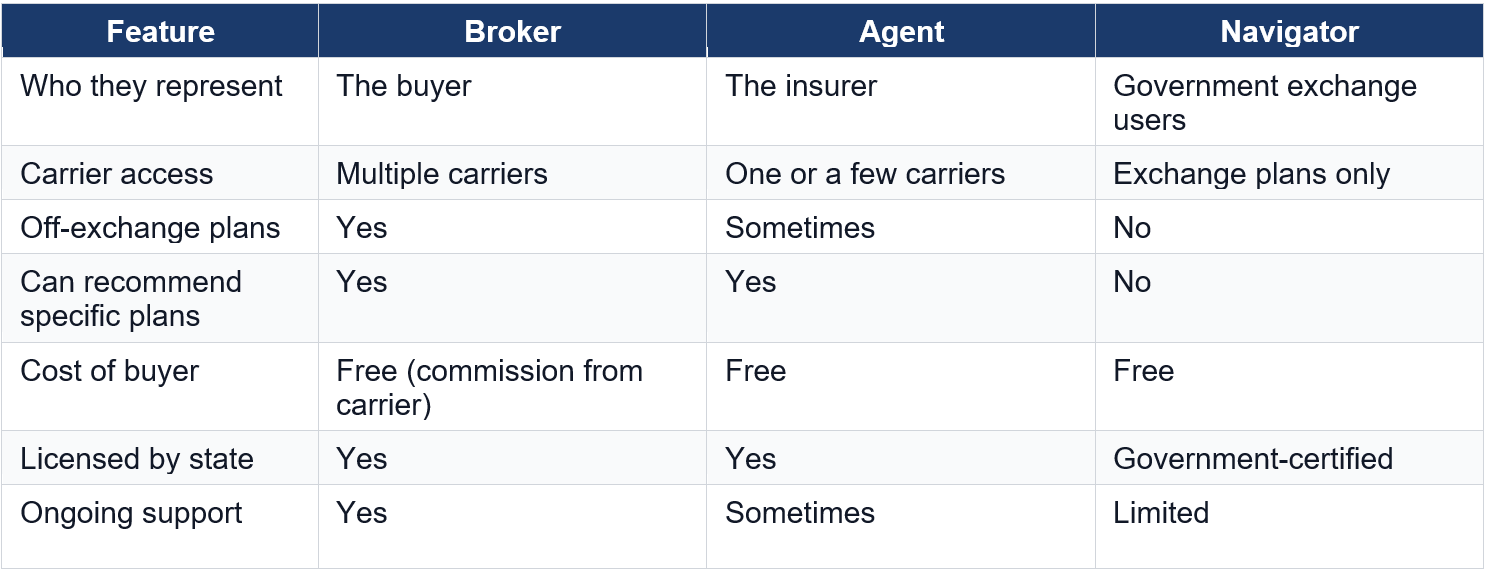

Health Insurance Broker vs Agent vs Navigator: Key Differences

These three roles are often confused and the distinctions matter. Here's how they compare:

Broker vs Agent

The most important distinction is who each person represents. An insurance agent represents the insurance company.They are contracted to sell that company's products. A captive agent only sells one company's plans. An independent agent may work with a few companies.

A broker, by contrast, legally represents you, the buyer. They have no obligation to any particular carrier and can compare the market objectively. In many states, brokers are required by law to recommend the plan that's in your best interest, not the one that pays the highest commission.

For a deeper look at these distinctions, see our full guide: Health Insurance Broker vs Agent — Key Differences.

Broker vs Navigator

Navigators are government-funded assistants who help people enroll in ACA marketplace plans. They are free, unbiased, and certified by the government but their scope is narrow. Navigators cannot recommend specific plans (they can only present options), they cannot help with off-exchange coverage, and they provide limited ongoing support after enrollment.

Brokers can do everything a navigator does, plus make specific plan recommendations and help with both on- and off-exchange coverage.

How Do Health Insurance Brokers Get Paid?

This is the question most people have and the answer matters because it removes the most common objection to using a broker.

Brokers are paid a commission by the insurance company after your enrollment is complete. This commission is already built into the premium you pay your premium is the same whether you use a broker or not. You do not pay more by using a broker. You do not pay less by going directly to an insurer.

In some cases, particularly for complex employer benefit plans, a broker may charge a consulting fee for services that go beyond standard plan selection (such as compliance auditing, employee education, or benefits strategy work). If a broker charges fees, they are required to disclose them upfront. Always ask.

Under the Consolidated Appropriations Act (CAA) of 2021, brokers working with employer group health plans with 50+ employees must now disclose their total compensation. This increased transparency helps employers understand exactly how their broker is being paid.

Who Should Use a Health Insurance Broker?

While anyone can benefit from a broker's expertise, certain situations make the value especially clear:

1. Individuals shopping for the first time If you've recently aged off a parent's plan, lost employer coverage, or become self-employed, the marketplace can be bewildering. A broker cuts through the confusion quickly.

2. Self-employed and freelancers: No employer plan means you're navigating the individual market alone. A broker shops the ACA marketplace and off-exchange options to find the best fit for your income and health needs.

3. Small business owners: If you want to offer health benefits to employees, a group health insurance broker manages the entire process: plan selection, employee enrollment, renewals, and compliance. Most small business owners don't have time to do this themselves.

4. People with ongoing health needs: If you have chronic conditions, regular prescriptions, or specific providers you need to stay with, a broker can verify plan compatibility before you enroll, preventing expensive surprises.

5. Anyone whose plan is renewing: Annual renewal is the most common time to overpay. Your insurer's renewal offer is rarely their best offer. A broker shops the market at renewal and can often find equivalent coverage at lower cost.

What a Health Insurance Broker Doesn't Do

It's equally important to understand the limits of a broker's role:

• A broker cannot sell you a plan that's not in their contracted portfolio. This is why some brokers may not show every option available in your market

• A broker cannot provide medical advice or predict what coverage you'll need

• A broker cannot override an insurer's decision on a claim, though they can advocate on your behalf

• A broker is not a licensed attorney and cannot provide legal advice on compliance matters

How to Choose a Health Insurance Broker

Not all brokers are equally qualified. Here's what to look for when selecting one:

Verify Their License

Every broker must be licensed by the state insurance department where they operate. You can verify a broker's license through your state's insurance department website. If you're shopping for ACA marketplace plans, they must also be certified with Healthcare.gov or your state exchange.

Check Their Carrier Contracts

Ask which insurance companies they're contracted with. A broker with a limited carrier list may not show you the full market. A well-established broker should work with most major carriers in your area.

Ask About Their Specialization

Some brokers specialize in individual health insurance. Others focus on group/employer benefits. Some work with specific industries (healthcare, dental, law, insurance agencies). A specialist will almost always provide better guidance than a generalist.

Ask How They're Compensated

A good broker is transparent about their commission structure. If they hesitate to answer this question, consider it a red flag. Since CAA 2021, compensation disclosure is legally required for most group plans.

Look for Reviews and References

Established brokers should have client testimonials, Google reviews, or references from current clients. Look for reviews that mention how the broker handled claims issues and renewals, not just initial enrollment.

Ready to find a broker in your area? See our guide: How to Find a Health Insurance Broker — including a full checklist of questions to ask.

The Role of Technology and Virtual Assistants in Modern Broker Practices

Today's health insurance brokers, particularly those running independent agencies rely on a growing stack of tools to manage their client load. AMS (agency management systems), CRM software, carrier portals, and compliance tracking tools have become essential.

Many growing broker businesses also delegate administrative tasks to virtual assistants professionals who handle the back-office work that consumes hours of a broker's day. From managing client renewals and tracking policy documentation to processing COI requests and following up with carriers, a trained insurance virtual assistant frees the broker to focus on advising clients and growing their book.

If you're a broker looking to reclaim administrative time, Savvital's insurance virtual assistants are trained on major AMS platforms and carrier systems and are available from $14/hr.

Frequently Asked Questions

Is it free to use a health insurance broker?

Yes. Brokers are paid by insurance companies via commission, which is already built into your premium. You pay the same premium whether you use a broker or buy directly. In some cases, brokers may charge consulting fees for advanced services, but standard plan shopping and enrollment is free.

What's the difference between a health insurance broker and an agent?

An agent typically represents one or a few insurance companies. A broker represents you — the buyer — and is contracted with multiple carriers. Brokers generally have a wider view of the market and a legal obligation to act in your best interest.

Can a broker help me with ACA marketplace plans?

Yes. Brokers certified with HealthCare.gov or a state exchange can help you compare and enroll in Qualified Health Plans on the marketplace — and can apply any premium tax credits or cost-sharing reductions you qualify for. They can also help with off-exchange plans, which navigators cannot.

Do I need a broker to get group health insurance for my employees?

You don't legally need a broker, but most small and mid-size businesses find them essential. A group health insurance broker manages plan selection, employee enrollment, renewals, and ACA compliance — saving HR teams significant time and often reducing the total benefits cost through better plan selection.

How do I find a licensed health insurance broker near me?

You can find licensed brokers through your state's insurance department, HealthCare.gov's 'Find Local Help' tool, NAHU (National Association of Health Underwriters), or through referrals from your accountant, attorney, or business associations. See our full guide: Health Insurance Broker Near Me.

Published on 9 Jul 2026

Author: Noor Ul Ain Liaqat